Contingency planning takes on a whole new meaning after the last two years as we have learned to be adaptable. Even better would be to anticipate issues that could occur and have a significant impact on our businesses. While we can’t always see everything coming, like the pandemic, we can be rigorous about thinking through potential scenarios that could be devastating and do what we can to mitigate the risks before they happen. In other words, the best way to manage threats to the business is to anticipate them so they can be proactively addressed.

That raises the question “What do most businesses need to be discussing as potential threats?” Would it surprise you to learn that according to a recent survey of 1600 C-suite executives across the globe conducted by The Conference Board, a members-driven business research group, that CEOs in the U.S. and Europe did not have Covid-19 at the top of the list? While it has not gone away, in the U.S. it is now ranked fourth. You might argue, and probably correctly, that it has led or at least contributed to the rise of the other challenges CEOs have identified as even higher priorities. Its impact will be felt for years to come. But remember, in some ways the changes it has forced are accelerations of already developing trends. At the very least it has increased the speed and scope of the issues we face.

First on the list? Labor shortages. Attracting and retaining talent must be a priority and it is requiring creative solutions, in addition to labor cost increases. Remote work is here to stay even if the pandemic fades as 53% of U.S. CEOs expect at least 40% of workers to remain remote (working at least 3 days a week outside the physical workspace). Part of the challenge facing U.S. businesses is how to maintain margins in light of upward wage pressure without changing the value provided to customers. If companies want to maintain profitability it requires re-thinking strategic value and how resources are deployed to create the highest return. Companies will have to stop performing historical activities that are not generating value.

Next, inflation. Although many economic experts have felt inflation is controllable, business leaders view it as top of mind as we face the coming year. In part aggravated by labor shortages discussed above, in addition to supply chain demand exceeding supply, costs are consistently being driven up across all sectors of business. The Wall Street Journal reported on January 14th that the U. S. Labor Department just revealed that inflation finished 2021 at its highest level since 1982 with the consumer price index up 7% in December compared to a year ago. While interest rates and other financial management techniques will occur at the federal level to try to slow its growth, businesses are passing on price increases. While customers are not thrilled, they appear to be accepting them as they are seeing these changes across the board and understand the economics behind them. The Conference Board survey revealed that 82% of global CEOs report upward price pressure on inputs into their business. In the U.S., 59% of CEOs expect inflation to be elevated until at least mid-2023 or beyond. It has been suggested by some strategists that now is a time we can safely evoke cost cutting tactics with the support of customers and the public, changing service offerings that have become common place. Examples abound, such as no cleaning services in hotel during your stay, the elimination of printed menus in restaurants, or new shipping requirements and priorities. Initiated due to Covid-19 some of these changes will be continued as customers adjust to the “new normal”, potentially carving costs out of the system to balance inflationary pressures and preserve profits.

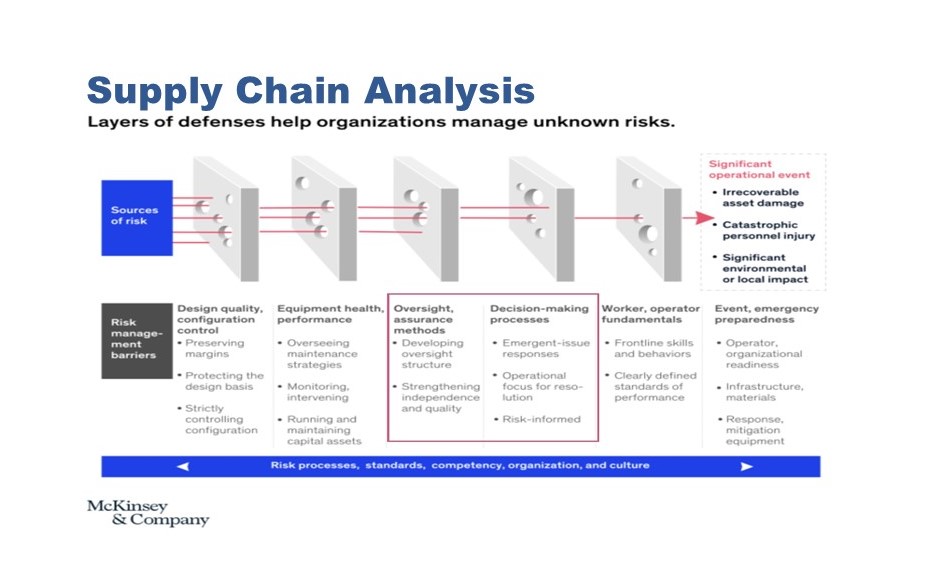

Supply Chain problems were ranked third. It is hard to meet projections for demand when you can’t get the items in stock to sell. No business likes to have to pull back on potential revenue due to lack of available parts (and workers). Manufacturers and retailers are pushing out delivery dates for ordered merchandise again and again. Customers are willing to pay higher prices for faster turnaround. In the short-term companies are trying to sell what they can supply (vs. what the customer wants) and hope the customer will substitute, while scrambling to find new sources to fulfill demand. Longer term, entire supply chain models are being reconfigured for less dependence on single sources, closer to home suppliers, and new processes that speed up reactions to potential threats. The chart below, from McKinsey, identifies the potential sources of risk for supply chains and ways to manage it. Those highlighted, oversight assurance and decision making, are a good place to start for those who have not yet evaluated the supply chain strategically.

As always, growth and performance success are a skillful combination of playing offense and defense. Most of my articles focus on offense but defense needs to be just as strategic. Every organizational leader in every sector needs to be assessing their highest risk and determining how to mitigate it before it becomes an issue. Identifying risks has elevated in importance not only in the C-suite but the Board room. Companies can’t afford to not anticipate those challenges that can derail the business. Has your organization identified its biggest threats for 2022 and taken action?